The Groove 262 - When Art Became an Asset Class

Welcome to the 262nd issue of The Groove.

I am Maria Brito, an art advisor, curator, and author based in New York City.

If you haven’t done so, please subscribe here, to get The Groove in your inbox for free every Tuesday.

When Art Became an Asset Class

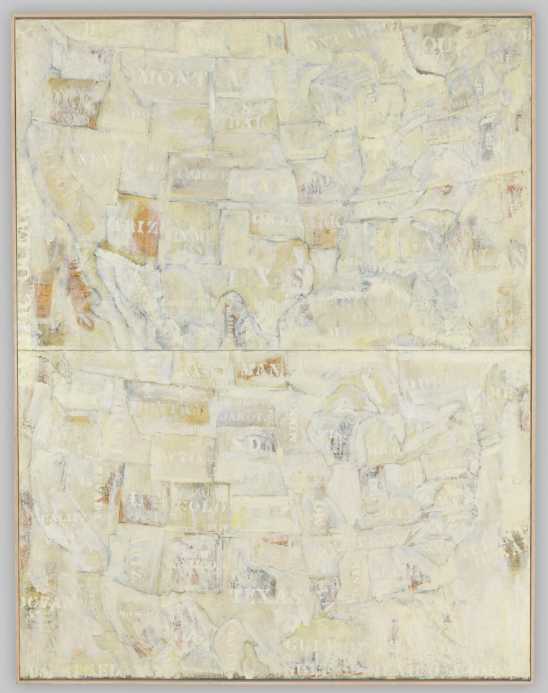

Jasper Johns’s Double White Map was bought by Ethel and Robert Scull in 1965 for $10,200 and sold for for $200,400 at an auction orchestrated by Sotheby Parke-Bennet in 1973.

Art didn’t become an asset class because artists started thinking like bankers. It became an asset class because everyone around the artist, i.e.: collectors, dealers, auction houses, and later economists, built the machinery to treat taste like a tradable signal. The shift can be marked by the moment the dinner-party talk moved from “Is it great?” to “What did it do last time it sold?”

And yet, “asset class” is a misleading phrase. It implies liquidity, comparability and standardization which are three things art resists by nature. The better way to frame it is this: art became an asset class when it became measurable enough to be argued about as an investment, and public enough to be benchmarked even if those benchmarks are imperfect.

The story is not one moment, but a sequence of inventions: the mega-dealer who sold Europe to America, the auction that taught contemporary art how to behave like a stock chart, the pension fund that tried to institutionalize taste, the Japanese bid that made the world stare, and the index that finally gave finance something it loves: a graph.

The Dealers Built the “Asset” Before Finance Did

Before art was an asset class, it was a status language and dealers were its translators. Joseph Duveen understood this better than anyone: “Europe has a great deal of art, and America has a great deal of money,” he famously observed. He then spent a career converting that observation into museum foundations and private empires for his clients, the likes of John Pierpont Morgan, Henry Clay Frick and Andrew Mellon. The trick was to sell not just paintings, but certainty: that some artists were “safe,” that some pictures were “A+,” that owning them meant joining the permanent class.

This is the first and most often ignored step towards art becoming an “asset”: the creation of categories. Old Masters. Impressionism. Modern. Postwar. Contemporary. Once a market has categories, it can have comparables. Once it has comparables, it can have narratives of appreciation. Dealers didn’t invent the love of art, but they professionalized the story that love could be stored in objects.

The result is what we still live with: the art world’s version of “blue-chip” wasn’t born at an auction. It was born in private conversations on velvet sofas, where a dealer told a collector not only what to buy but also what the future would eventually agree was important.

The Auction That Taught Contemporary Art to Trade Like a Market

If you want one night that made contemporary art behave like an asset class, it’s October 18, 1973 - the Robert and Ethel Scull sale at Sotheby Parke-Bernet. It wasn’t the first time art sold at auction, obviously. But it was the first time a major single-owner sale of living American artists made the public understand that contemporary art could “perform.”

Prices didn’t just rise; they multiplied dramatically. A Cy Twombly sold for $40,000 after Scull had paid $750; Jasper Johns’s Double White Map brought $240,000 after a $10,200 purchase. Those numbers look quaint now, but the psychological effect was huge: artists and collectors watched their private world turn into public price discovery. This was the moment contemporary art started to acquire the emotional charge of a financial instrument: profit, envy, timing, regret.

The Scull sale created scorekeeping. Once the scoreboard is public, you get new behavior: flipping, career engineering, the fetish of records, the idea that the “right” artist is the one whose price graph goes up. Aesthetic arguments didn’t disappear, but instead they started sharing oxygen with numerical ones.

Institutions Tried to Formalize It, and Finance Tried to Quantify It

The most literal “art as asset class” experiment came in 1974, when the British Rail Pension Fund started buying art, eventually deploying about £40 million (roughly 3% of holdings at the time) with Sotheby’s involved. This was a pension fund trying to do what collectors always did: buy beauty, prestige, and scarcity, but inside an institutional logic of allocation and return. It was both audacious and oddly revealing: if a pension fund is collecting, then the culture has already started to treat art as a financial category, not just a cultural one.

Then came the high spectacle of the late 1980s and early 1990s: record prices that made headlines feel like earnings reports. Van Gogh’s Irises sold for $53.9 million at Sotheby’s New York in 1987 (buyer: Alan Bond). In 1990, Van Gogh’s Portrait of Dr. Gachet hit $82.5 million at Christie’s New York (linked to Japanese buyer Ryoei Saito). These were cultural announcements, pronouncing that art could absorb the same mania as any other scarce trophy.

Finally, the economists arrived with tools that made finance feel at home: indices. The Mei Moses methodology, later acquired by Sotheby’s and branded “Sotheby’s Mei Moses,” uses repeat sales to track changes in value, an attempt to create a market “thermometer” for art. It is imperfect, like all art-market data, but the symbolic shift matters: the moment you can plot art, you can pitch it.

Is Art a Real Asset Class?

So, when did art become an asset class? Not when someone first paid a fortune for a masterpiece. Not even when a collector boasted about “investment.” It happened when the system evolved and art could be classified, benchmarked, scored, and narrated as performance. Where those narratives could travel faster than the objects themselves.

The irony is that treating art like an asset has always been a category error. Art is illiquid, idiosyncratic, and stubbornly emotional. But the desire behind the asset-class story is real: people want beauty that also holds value, culture that also signals power, objects that can do double duty as pleasure and storage.

That’s why this language never goes away. It’s not that art became finance. It’s that finance learned how to talk about art and the art world learned how to sell that conversation.